But what about the deductible? Deductible is the amount you’ll pay before your insurance policy starts to pay benefits for covered services.[0] Higher deductibles typically result in lower premiums and vice versa.[1]

And then there are high-deductible health plans (HDHPs). In the remainder of this blog post, we’ll cover:

- Deductible costs over time and why they’re going up

- What a qualifying HDHP actually is, including the 2020 limits

- Some ideas for help covering your deductible costs

More High Deductible Health Plans, Higher Deductibles Today

According to CDC data, the trend from the last 10 years has been increasing enrollment in high deductible health plans (HDHPs), both individual health plans like the ones available on the Affordable Care Act (ACA) Marketplace, and group plans, like those offered through employers.

The table below shows that the percentage of people with high deductible private health coverage under age 65 (both with and without health savings accounts (HSA)) has increased from 25.3% in 2010 to 47% in 2018.[2]

| 2010 | 2014 | 2018 | |

| HDHP without HSA | 17.6% | 23.6% (+6%) | 25.7% (+2.1%) |

| HDHP with HSA | 7.7% | 13.3% (+5.6%) | 21.3% (+8%) |

| Total | 25.3% | 36.9% (+11.6%) | 47% (+10.1%) |

On average, individual ACA plan deductibles have gone up from $2,240 back in 2014 at the start of the ACA to $3,149 in 2020, an increase of 29%.[3] Not only have high deductible health plans become more commonplace but health insurance costs, in general, tend to increase each year, alongside healthcare costs.

For more help understanding health insurance deductibles in general, check out “Health Insurance Deductibles 101.”

What is a Qualified High-Deductible Health Plan?

Just because a health plan has a high deductible doesn’t mean it’s considered a qualifying high deductible health plan per IRS guidelines.

“Qualifying” or “HSA-qualifying” high deductible health plans are narrowly defined by the IRS to meet a specific set of criteria as follows:[4]

- Be an ACA-qualifying plan like individual major medical insurance or an employer’s qualifying health plan.

- Meet the deductible thresholds as defined by the IRS (shown for 2019 and 2020 below).

- Have an out-of-pocket calendar year maximum limit that does not exceed the amount specified by the IRS (shown for 2019 and 2020 below).

HDHP Minimum Annual Deductible Amount

| 2019 Calendar Year[5] | 2020 Calendar Year[6] | |

| Individual | $1,350 | $1,400 |

| Family | $2,700 | $2,800 |

HDHP Out-of-Pocket Maximum Limit*

| 2019 Calendar Year[7] | 2020 Calendar Year[8] | |

| Individual | $6,750 | $6,900 |

| Family | $13,500 | $13,800 |

*Applicable to in-network services only

Just because a plan meets the above criteria does not automatically make it an HSA-qualifying HDHP as there are other plan characteristics that could disqualify a plan that otherwise meets the deductible and out-of-pocket amounts.[9]

So how do you know if you have a health plan with a high deductible or an HSA-qualifying high deductible health plan? The best way to know for sure is to look for a designation indicating the health plan as “HSA-eligible”[10] or to call your insurance provider and ask.

When Should You Get a Health Plan With a High Deductible?

As mentioned earlier, it may be difficult to avoid a plan with a high deductible,[11] particularly if you’re not a high income earner that can afford a plan with a higher monthly premium payment.

An ACA health insurance plan with a higher deductible may be okay if you’re generally healthy and primarily use in-network basic preventive care, which is not subject to a plan’s deductible according to ACA guidelines.[12]

However, a HDHP could be a problem if you need to use your health insurance for other types of services that are subject to your deductible, like hospitalization.

- 51% of people with a HDHP reported skipping or postponing care due to cost[14]

- 34% of people with health insurance (not just those enrolled in HDHPs) had difficulty affording their deductible[15]

- 40% of workers with employer-sponsored HDHPs had difficulty affording healthcare, insurance, or paying medical bills[16]

Learn more about the ACA’s cost-sharing metal levels, including how to decide which option may be the best fit for your healthcare needs and budget.

Enrolling in or Already Have a High Deductible Health Plan?

ACA Subsidies

If you’re shopping for individual major medical insurance either during a special enrollment or open enrollment period, you may want to see if you qualify for one or both ACA subsidies:

- Cost sharing reduction

- Premium tax credit

A cost-sharing reduction (CSR) helps lower out-of-pocket costs when you need to obtain healthcare. This subsidy is only available when enrolling in a silver-level health plan.[17]

Another way to lower your deductible is if you qualify for a premium tax credit to reduce your monthly premium costs. Due to the subsidy offsetting part of the premium cost, you may be able to afford a plan with a higher premium and lower deductible than you would have without the subsidy.

Learn more about income limits to qualify for ACA subsidies.

Use the ACA calculator to see if you could qualify for a federal subsidy.

When viewing health plans on the Healthcare.gov marketplace, you’ll see color-coded labels for HSA- and CSR-qualifying plans, as well as an indication of the before and after premium amount when you qualify for a premium tax credit.

If you want to be able to use an HSA with your high deductible health plan, make sure to look for the blue “Eligible for a Health Savings Account” label when reviewing plans[18] as shown in the second and third images, below.

CSR + Tax Credit Eligible

HSA Eligible

Premium Tax Credit + HSA Eligible

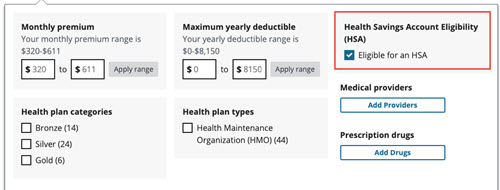

In the ACA Marketplace, you can also apply a filter to view only HSA-eligible plans on your results page, as shown below.[19]

Filter Options

Supplemental Medical Gap Insurance

Whether or not you have a qualifying HDHP, a supplemental medical gap health plan may be able to help by providing additional lump-sum payments when a covered accident or illness occurs.

As non-ACA-qualifying health plans, they work alongside your major medical coverage but do not coordinate with it. This type of plan does not qualify as minimum essential coverage under the ACA. You can use the additional benefits to help pay your major medical health insurance deductible, medical expenses, household expenses, and more. Learn more about gap insurance, including how it works.

Compare gap health insurance costs and plans by requesting a quote.

Want to Cancel Your High Deductible Health Plan?

If your health insurance costs are too high, whether that’s premium, out of pocket costs, or both, you’ll need to carefully consider if you should maintain your policy or cancel it.

Remember, some states have individual mandates and tax penalties if you go without qualifying health coverage.

Then make sure you understand your options for healthcare when you’re uninsured, and consider if a non-qualifying plan, like short term medical, may be a wise choice to provide some level of benefits (after the plan’s deductible is met) while you’re temporarily between ACA plans. Learn more about short term health insurance. This type of plan does not qualify as minimum essential coverage under the ACA.

Request a quote to compare premium and deductible costs for short term health plans.

Get a Short Term Medical Quote

Summary + Next Steps

We’ve covered a lot of information about high deductible health plans, including:

- What is a HDHP, what about a qualifying HDHP?

- Deciding if you should enroll in one or cancel your existing HDHP

- How to identify an HSA-qualifying health plan on Healthcare.gov

- Using ACA subsidies, an HSA, or a medical gap plan with your HDHP

- Options if you can no longer afford your high deductible health plan

Now that you’ve got a comprehensive understanding of high deductible health plans, here are some next steps to consider:

- Enroll in an HSA-qualifying HDHP and open an HSA.

- Use ACA subsidies if you qualify for them.

- Add supplemental gap insurance for additional benefits that can help with your major medical policy’s out of pocket costs, including the deductible.

- Call (888) 855-6837 to speak with a health insurance agent to help you understand your options.