Knowing what your family health insurance options are is an important step, right up there with picking out nursery colors and stockpiling diapers!

First, we’re going to discuss some of the child-related costs you’ll likely run into if you have children in your family, in case you’re on the fence about getting family coverage. We’ll also cover who can be on your family policy – can you add your stepdaughter or stepson?

Then, we’ll discuss your family health insurance options, including:

- Employer-sponsored (group) family health insurance plans

- Individual family health insurance plans from the ACA exchange or private marketplace

- Government-sponsored coverage: Medicaid or CHIP

Know you need family health insurance? Jump right to the options you can consider.

How Expensive Are Kids?

Adding children to your family is expensive!

The most recent and widely cited study is from 2015, and estimates the cost of raising a child from birth through age 17 (not including college) at $233,610 – or $14,000 a year.[0]

Costs will vary depending on a number of factors:

Housing + where you live: whether urban or rural and where in the country. About 26-33% of the total cost is related to housing.[1]

Childcare, education + food: These are the next highest expenses for families with kids. Food makes up about 18% of total costs and child care/education 16%.[2]

Your household income: Lower-income families understandably spend less than the average, around $174,690 per child, with higher-income families spending over twice as much, around $372,210 per child.[3]

Finally, your annual costs for food, clothing and healthcare tend to grow as your child grows.[4]

It’s important to plan for the high costs associated with raising kids, and family health insurance may be part of that plan!

Children’s Healthcare Costs

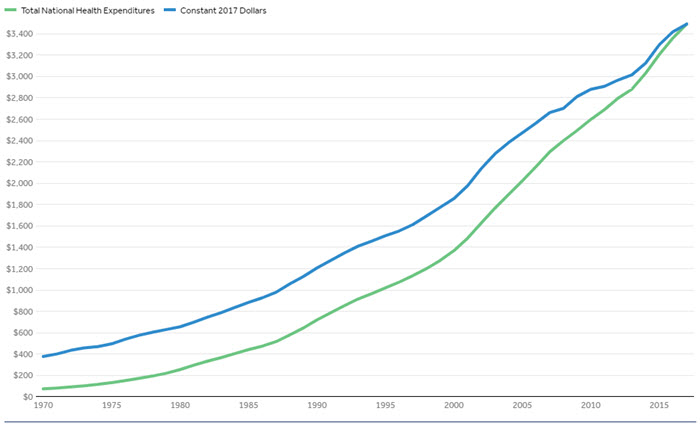

Healthcare is expensive, and healthcare spending in the U.S. is consistently on the rise.[5]

On a per capita basis, health spending has increased in the last four decades from $355 annually per person to $10,739 in 2017 (health spending includes costs of both healthcare and health-related activities such as administration of insurance, health research and public health).[6]

U.S. Total National Health Expenditures per capita (1970-2017) Peterson-Kaiser[7]

According to the Centers for Medicare and Medicaid Services, in 2014 (the most recent year data is available), personal healthcare spending per child was $3,749.

That year, children accounted for approximately 24% of the population and about 11% of all personal healthcare spending.[8]

Kids’ health conditions with the highest associated spending (2013) were:

- Inpatient newborn care

- Attention-deficit/hyperactivity disorder

- Dental care (including checkups and orthodontics)[9]

Covering everyone in the family is the best option if you can afford it. However, if you’re looking for insurance only for your child, there are options.

Family Insurance Costs

According to 2017 data from the Peterson-Kaiser Household Spending Calculator, the typical non-elderly family of four with an “average” income ($79,630) purchasing coverage in the ACA marketplace pays more in total spending and out-of-pocket costs (copays, deductibles, coinsurance) as health status of one or more family members worsens.

Household Health Spending (2017)[10]

| Better Health[11] | Average Health[12] | Worse Health[13] | |

| Total Spending | $15,900 | $16,050 | $20,450 |

| Percent of Household Income | 20% | 20% | 26% |

| Premium Portion | $7,700 | $7,700 | $7,700 |

| Out-of-Pocket Portion | $4,700 | $4,800 | $9,250 |

“Worse” health can come in the form of a chronic condition. Obesity alone affects almost 1 in 5 children and 1 in 3 adults, putting them at risk for other chronic diseases including diabetes and heart disease.[14] Obesity costs the US healthcare system an estimated $147 billion a year.[15]

Healthcare Benefits for Children

While healthcare spending increases as children age,[16] babies and school-age children tend to require a lot of preventive care in the form of screenings and vaccination. These are healthcare services that are considered essential health benefits that are part of all ACA-qualifying major medical insurance plans.

Childhood Development

All infants, children, and adolescents should have regular well-child checkups in order to establish a good foundation for proper growth and development.[17]

Remember, a health issue may not have outward symptoms early on, so regular visits can help identify potential medical issues so your child can get treatment as early as possible.[18]

Babies are usually checked by a healthcare provider within the first week of going home from the hospital. Visits are recommended at two, four, six and nine months.[19]

Visits are then recommended at:[20]

- 12 months

- 15 months

- 18 months

- 24 months

- 30 months

- Annually from 3-17 years

Vaccines

The Centers for Disease Control and Prevention (CDC) recommend around 10 different vaccines for a child from birth to 15 months to prevent highly infectious and serious diseases like: chickenpox, diphtheria, hepatitis A and B, haemophilus influenza type b, measles, mumps, pertussis, polio, pneumococcal pneumonia, rotavirus, rubella, and tetanus.[21]

CDC Recommended Child and Adolescent Immunization Schedule (2019)

In addition to scheduled preventive care, babies, toddlers and school-aged kids tend to experience recurring conditions like colds and ear infections at a much higher rate than older kids or adults.

Colds

Starting at about six months of age, babies, toddlers and preschoolers get around 7-8 colds per year. At school age, it goes down to around 5-6 colds per year. And as teenagers they finally reach an adult level of immunity with around 4 colds per year.[22]

Ear Infections

Ear infections are so common in children that 5 out of 6 kids will have at least one ear infection by their third birthday. And ear infections are the most common reason parents bring their child to a doctor.[23]

Having comprehensive major medical family health insurance means you can visit your pediatrician or even the urgent care, if necessary, without having to worry about paying the total cost out-of-pocket.

Who Can Be Included on Your Family Health Insurance Plan?

The word “family” means different things to different people. Here are some family scenarios outside of the common parent/biological child household, one of which may apply to you.

Can I add my stepchild to MyHealthInsurance.com? Sometimes. Employer group health insurance plans do not have to cover stepchildren. If you buy a health insurance policy through the federal marketplace or your state’s exchange, if you can include the child on your tax return as a dependent you can add them to your health insurance.[24]

Can I add my adopted son or daughter to MyHealthInsurance.com? Yes. Adopting a child qualifies you for a special enrollment period under the ACA, during which time you can shop for new health insurance for your family.[25] Additionally, once your child’s birth parents have officially consented to the adoption, you can request the child be added to your existing health policy. Make sure you change your policy within 30 days of placement.[26]

Can I add a parent to MyHealthInsurance.com? Probably not. Very few insurers allow you to add a parent to your family health insurance policy as dependents and those that do require that your parent meet certain requirements such as that they’re living with you and you’re providing for them financially.[27]

Can I add my girlfriend or boyfriend to MyHealthInsurance.com? Maybe. Couples of the same and opposite sex are able to share insurance under a domestic partner insurance coverage. Since there are no current federal guidelines that state what a domestic partnership is, that answer is up to each individual state. More than a dozen states mandate that employer-sponsored group health insurance plans provide benefits for domestic partners if they provide them for spouses.[28]

Can I add my fiance to MyHealthInsurance.com? The same domestic partnership considerations above would apply.[29]

Options for Family Health Insurance

There are three main options for family health insurance plans:

- Employer-sponsored family health insurance plans

- Individual family health insurance plans

- Government-sponsored programs: Medicaid or CHIP coverage

There are also supplemental health insurance options that may help make accessing healthcare more convenient or help with out-of-pocket costs associated with your major medical coverage.

Employer-sponsored family health insurance plans

If your employer offers health insurance that’s often the first place to look for coverage. Check to see if the price/coverage offered are the best fit for your family’s needs.

Even if you have access to employer-sponsored insurance, you may still buy more affordable family health insurance plans on the Marketplace that’s less expensive or offers better coverage for your family if you meet certain criteria. One thing to be aware of with an employer-sponsored family plan is the ACA’s “family glitch.”

The ACA’s “Family Glitch”

The ACA’s “family glitch” impacts somewhere between 2 to 4 million people who have access to employer coverage that they can’t afford, yet they do not qualify for subsidies from the ACA marketplace to help them obtain more coverage.[30]

The “glitch” is the result of how the ACA’s defines “affordable” coverage.

Employer coverage is considered “affordable” by the ACA if the cost to cover the employee only is less than a specified percent of the employee’s annual household income (9.86% as of August 2019) – even if the actual cost to cover the entire family is much higher, as is typical.[31]

And if that employee has access to what is technically considered “affordable” insurance through their employer (not taking into account one or more additional family members) they are not eligible for subsidies if they purchase health insurance from the public exchange.

Here’s an example:[32]

A construction worker who makes $66,000 can get employer-sponsored coverage for $172 per month in premium for just himself, which, at 3.1% of his income, is well under the ACA’s affordability threshold of 9.86%.

Adding his wife, who is a stay-at-home mom, and daughter to the coverage would cause the monthly premium to go up to $1,060, which is just over 19% of the household income!

The example family premium used above is not unrealistic. For 2018, the average family monthly premium for an employer-provided group plan was $1,635.[33]

A family individual major medical policy

If you don’t have access to an employer-sponsored plan you may be able to get a family major medical policy through the ACA exchanges or private marketplace outside of the annual open enrollment period if you qualify.

If anyone in your household has had a baby or adopted a child within the past 60 days, you may qualify for a special enrollment period.[34]

When you enroll in or change policies with a special enrollment period, your new health coverage can start the day your baby is born – even if you enroll in the policy up to 60 days afterward.[35]

Remember, the only way to get subsidies for ACA-qualifying health insurance is to enroll through the public exchange.

Learn more about qualifying for a special enrollment period, and find out where to shop for ACA coverage depending on your state.

Medicaid or CHIP

Depending on your household income, you may qualify for free or low-cost health coverage from Medicaid or the Children’s Health Insurance Program (CHIP).

You can apply for Medicaid with a Medicaid agency or through the marketplace any time during the year.[36]

Eligibility qualifications vary between Medicaid and CHIP.[37] Children raised in families earning 133% or less of the federal poverty level per year are eligible for Medicaid.

The CHIP program was established to expand coverage to children who have lower family incomes, but are higher than the Medicaid level.[38] In most states that threshold is set at 200% of the federal poverty level.[39]

Check to see if you qualify at Healthcare.gov.

Short term health insurance

If you missed your special enrollment period and need temporary coverage for a new family member or the entire family, you may want to consider a short term medical policy.

Short term policies offer you and your family a range of healthcare benefits to help pay for unexpected medical expenses.

However, it’s important to understand that these are not ACA-qualifying policies. That means they are not guaranteed-issue, and do not cover the essential health benefits, including all the preventive care, screenings and vaccinations you’ll want your child to have access to.

Short term health insurance premiums are generally less expensive than major medical premiums because these policies include less coverage and are effective for a limited period of time (from 30 to 364 days depending on where you live).

Premiums for short term health insurance will vary depending on the benefits you select. Some examples of medical expenses short term health insurance may cover include:

- Inpatient and outpatient hospital care

- Intensive care

- Emergency room visits

- Ambulatory services

- Surgical services

- Certain pre-existing conditions

Find out what short term coverage could cost you.

Get a Short Term Medical Insurance Quote

It is also possible to combine multiple non-ACA policies if you identify potential gaps in your healthcare coverage. For instance, you might enroll in a short term policy as well as dental insurance and telemedicine to get access to more benefits and coverage.

Supplemental Insurance + Telemedicine

By most measures, major medical health insurance is expensive. And the out-of-pocket costs that you’re responsible for before your policy will begin to pay a portion of your covered expenses generally rises every year, whether you have an employer’s plan or have purchased your own coverage.[40]

There are supplemental health insurance policies that can help provide coverage that may be missing from your major medical plan, as well as help cover your out-of-pocket costs when it comes time to use your insurance.

Dental insurance provides benefits that help pay for a range of dental services that your major medical policy does not cover, from preventive to major care. Learn more about dental insurance.

If you have an ACA-compliant major medical insurance policy, it includes dental care for children as an essential benefit, but you may need to buy stand-alone dental plans for the adults in your household.

Telemedicine includes access to virtual health consultations with licensed physicians 24/7/365. Telemedicine can help make treatment more convenient for non-critical and/or recurring issues, especially the kinds of conditions kids seem to be prone to, like ear infections or colds. Telemedicine is not insurance. Learn more about telemedicine.

Add supplemental gap insurance or hospital indemnity to your major medical policy to help with out-of-pocket costs.

Gap health insurance pays a lump sum benefit when a covered accident or illness occurs. This benefit can then be used towards your major medical deductible payment or for other expenses like groceries, transportation, and housing. Learn more about gap health insurance.

Hospital indemnity insurance can supplement your major medical policy by providing additional fixed indemnity benefits that payout on a per period or per-incident basis. Hospital insurance does not coordinate benefits with other insurance policies and does not count as qualifying minimum essential coverage. Learn more about hospital indemnity insurance.

Summary + Next Steps

If you have a family or are considering starting one, getting health insurance coverage for everyone is important. There are a number of options to consider:

- Employer-sponsored group plan if you have access to one and it fits your family’s needs. And budget.

- An individual ACA-qualifying major medical family plan from the public exchange (subsidies may be available) or private marketplace.

- Medicaid for the family or CHIP coverage for your children if you qualify.

Remember, a supplemental health insurance policy could help to either round out your coverage or increase your benefits by providing either a lump sum or fixed indemnity benefits that you can use to help pay for your major medical deductible, coinsurance and other healthcare costs that may not be covered by your policy.

Finally, if you aren’t able to obtain major medical insurance right now, a short term medical policy may be able to help with your medical expenses relating to hospitalization or emergency care.